Equity markets had a turbulent year in 2022 with the Russia-Ukraine war, rising interest rates and the resurgence of COVID-19-related restrictions in China impacting investor confidence. For investment banks, the strength in investment banking in 2021 eased in 2022 due to market headwinds. That said, the high volatility was a boon to trading desks, especially for fixed income trading.

2023 looks set to be an interesting year for sell-side research houses. On one hand, the focus on active investing, expectations for receiving expert opinions and corporate access are likely to keep sell-side analysts in high demand. On the other hand, investment banking activity is expected to remain subdued, putting pressure on research budgets. Technology is also playing its role in both producing and disseminating research. Research heads and COOs would play a crucial role in balancing costs and revenue opportunities.

Nevertheless, there are signs of inflation easing and a slower pace of rate hikes. The gradual improvement in investment banking activity in the second half of 2023 and continued strength in trading activity are likely to push demand for sell-side research higher in 2023.

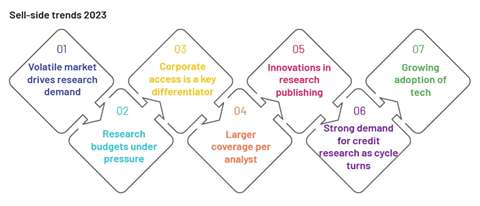

We expect the following themes to play out in 2023 and beyond in the sell-side research space

Sell-side research and analysts are likely to remain in demand as active investors look for alpha in a murky economic and financial environment

The investor community searched for answers all through 2020-21. First, due to the immediate economic shutdown driven by the pandemic in 2020 and then the sudden V-shape recovery led by quantitative easing and government efforts in 2021. 2022 was not very different, with the outbreak of a much-feared war, rising inflation and supply-chain disruptions. Through this tumultuous period, sell-side research regained its old shine and more as investors sought expert opinions and stock-picking ideas.

Through the latter half of 2022 and into 2023, equity markets have been impacted by rising inflation, higher interest rates and recession fears. This has led many investors to shift focus from a passive approach to active investing. Based on Goldman Sachs data through mid-November 2022, about 55% of actively managed funds were ahead of their respective benchmarks, the largest share since 2007, when 71% of funds beat their benchmarks.

Research budgets to remain under pressure

Most investment banks have announced headcount reductions in late 2022 and early 2023 to manage costs and reflect lower investment banking activity. While most of the headcount reductions have been focused on the investment banking side due to lower deal volumes, other areas including research have been impacted. Managing headcount (hiring freezes, layoffs, resignations) and research budgets would be the key focus area for research heads and COOs in 2023 as they look to maintain and grow support for their clients.

Research operations would be under pressure to streamline pain points in internal processes and drive client engagement. They also need to ensure compliance in reporting related to MiFID II, which has become further complicated due to the increasing number of client touch points and complex fee structures.

Ability to provide effective corporate access will decide Institutional Investor (II) rankings

In volatile markets, investors look for opportunities to meet with company management teams and participate in industry conferences, seeking new information and updates to adjust their investment theses. 2023 is likely to require more of this as companies adjust their strategies, plans and estimates amid a high-inflation and high-interest-rate environment, easing supply-chain issues, China opening up and an ever-evolving geopolitical backdrop.

We expect sell-side research houses to invest in enhancing their corporate access capabilities and event offerings. As pandemic-related fears recede, in-person meetings and conferences have also returned to pre-pandemic levels. Moreover, as investment banking deal volumes slow, sell-side research firms would look for ways to grow engagement with corporates and the buy side.

Breadth of coverage to increase as reports become shorter and are published more frequently

As economic and market volatility remains high and sectors come into and go out of favour quickly, firms are expected to increase the breadth of sectors and stocks that are covered. For example, tech valuations have been under pressure recently, and investors are rotating towards other sectors such as energy and retail to find better returns. The increasing number of economic, financial, market, geopolitical and industry events since 2020 has also led to more frequent report updates, although the average size of report has reduced. Real-time analysis and expert opinion are favoured by investors and would drive the trend in 2023.

We also see growing coverage of small/mid-cap stocks at sell-side banks and independent research firms as corporates look to attract investors to their stocks through regular publications.

Innovation in research publishing and consumption to continue

The increase in information available and an inadvertently reduced attention span have forced research houses to look for innovative ways to connect and engage with their clients. The advent of technology has helped push both the supply and demand sides of this. Sell-side research firms are increasingly using technology to package and disseminate research.

Pioneers are using infographics, podcasts, short videos, flash notes, push notifications and other ways to get clients’ attention. We expect an increasing number of firms to use such favourable tactics and innovate further.

Credit research – a key area of focus for the sell side as new issuance and investor demand recover in 2023

Global bond markets had a strong start to 2023, with record new-debt sales in Europe and emerging markets. Refinitiv data shows that emerging-market governments issued USD61bn in international bonds in January 2023, the most since 1970. European governments sold USD75bn in bonds, while investment-grade companies issued bonds at the fastest pace since 2011. This is in stark contrast to 2022, when investor confidence in emerging markets and Europe was impacted by the Russia-Ukraine war and rising commodities prices. Investors expect the bond market to be more favourable in 2023, as market participants believe that inflation and the interest rate cycle are close to their peak.

Increased adoption of tech in sell-side research

AI tools such as ChatGPT could aid analysts in secondary research, daily/weekly notes, data analysis and drafting earnings reports. That said, there is still no substitute for deep sector understanding that can help identify factors impacting a company or sector. While investors will be wary of depending exclusively on AI analysis and recommendations, this could help improve the research process in the hands of an experienced analyst.

How Acuity Knowledge Partners can help

We have 500+ analysts supporting around 60 sell-side research firms in research, publishing and operations. Global investment banks and other research firms leverage our experience to rapidly increase internal analyst bandwidth and expand coverage in equities and credit. We set up dedicated teams of analysts (CAs, MBAs and CFAs) to support our clients on a wide range of activities including idea generation, building financial models, financial analysis, thematic research, building databases and providing regular sector coverage. On the publishing side, we help clients with supervisory analyst, editorial, design and formatting support. We also support research operations in areas such as CRM, broker votes, corporate access, and expense and invoice management.

About the Author

Geo John, CFA

Geo John has over 14 years of experience in equity research, team management and training. Since joining Acuity in 2013, Geo has covered multiple sectors including TMT, Payments, Consumer and Energy. In his current role, he is responsible for setting up new teams and managing existing Equity Research delivery teams. Prior to Acuity, Geo worked as an Equity Research analyst at Goldman Sachs for more than four years, based out of India and US. Geo holds an MBA from Indian Institute of Science, Bangalore (India) and a B.Tech degree in Electronics and Communication Engineering from University of Kerala (India). He is also a CFA charterholder.